By Mark Shore

Understanding the characteristics of a given investment space helps one to understand and appreciate that given space. This article discusses some of the statistics of Peer-to-Peer loans (P2P), thus developing a better understanding of P2P lending.

There is a myth that P2P borrowers are all subprime level borrowers. However as noted in the paper “P2P Lending for Institutional Investors and Wealth Managers: An Overview” not all borrowers are accepted onto a P2P lending platform. Prosper and Lending Club developed standards and policies of vetting and underwriting loans with an estimated 90% rejection rate.1 Prosper and Lending Club tends to concentrate on borrowers with a Fico score of 640 or better, also known as prime and near-prime borrowers.2

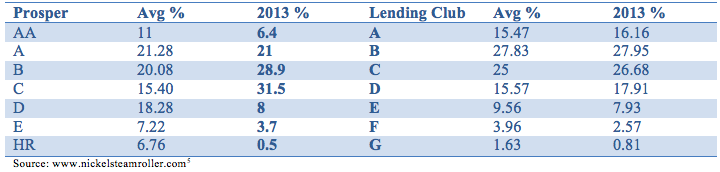

Prosper and Lending Club, the two largest P2P U.S. platforms utilize a seven level grade default risk ranking system to determine an appropriate interest rate for the given loan. This is similar to the rating process of banks or investment rating agencies.

According to the Federal Reserve System, the seasonally adjusted charge-off for credit cards averaged 3.44% in 2013. 3 The default rates of P2P lending vary by ranking from about 1% to 6%.4 However in some cases during the financial crisis the default rates reached 30%. The vetting process of loans has evolved since the early days of P2P lending and from the experience of the financial crisis.

Table 1: The average percentage of loans per year of each rating category for Lending Club from 2007 to 2013 and Prosper from 2009 to 2013 and the percentage for December 2013.

As Table 1 points out, the majority of the P2P loan origination is in the first three grade rankings of both platforms. Therefore the majority of the P2P loans are of higher quality.

According to Lending Club data, loans listed between December 2011 and December 2013 had the following statistics: The average income was $72,239, maximum income was $7,141,778. 3.43% of the income was $25,000 or less. 0.08% of the income levels were above $500,000. The majority of the income levels were between $26,000 and $100,000.

Chart 1: Distribution of borrower’s income levels between December 2011 and December 2013

The average number of years of a borrower’s current job is 6.16 years. 31% of borrowers maintained their job for 10 years or more. 57% of the borrowers are home owners. The loans are relatively short term as 76% of the loans have a term of three years. The average loan was $14,071 with a maximum loan of $35,000 and a minimum of $1,000.

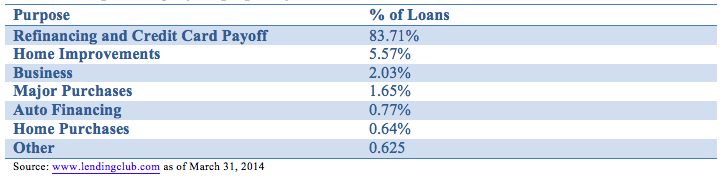

Table 2: The percentage of the purposes for the loans

Table 2 notes, over 83% of the loans are for the purpose of refinancing and credit card payoff as the borrowers are seeking to reduce the leverage of their balance sheet.

“We focus our efforts on acquiring the best risk adjusted loans on the platform” says Don Davis, managing partner of Prime Meridian Income Fund, a P2P lending fund. “One of our primary objectives is to be able remain profitable for our investors even if the default rate on our entire portfolio doubled during a recession.”

In summary, the data shows, the majority of the loans are for the purpose of credit card payoffs and refinancing over a 3 year period. The average borrower’s income is above $70,000. The borrower tends to have job stability and the rejection rate of loan applications is high. The majority of the loans tend to be ranked in the three highest grade levels. Therefore, the characteristics of the loans tend to be originated from prime borrowers. Past performance is no guarantee of future results.

1 Peer-to-Peer Lending Opportunities Opening up for Advisors , Bill Kassul, 1/18/2014 wealthmanagement.com

2 Loans that Avoid Banks? Maybe Not. Amy Cortese 5/3/2014 New York Times

3 http://www.federalreserve.gov/releases/chargeoff/chgallsa.htm

4 P2P Lending pulls in big investors – should you bite? A. Feldman, Beth Pinsker; 8/27/2013 Reuters

5 The averages were derived from the December data of each year