Fixed income yields are terrible right now. You know you need to build a portfolio of more than just stocks to properly manage risk. The best portfolios have different asset classes in them that don’t correlate with each other, aiding us in proper risk management. Both stocks and fixed income in a portfolio are the basis of Modern Portfolio Theory.

With these horrible yields in fixed income, how do you accomplish this in today’s market and make money?

The New Fixed Income Option

Marketplace/Peer to Peer Lending is a relatively new arrival as an asset class but it has some very important fixed income characteristics, especially in this low interest rate environment that we have been in for quite a few years now.

Many people are intimidated by Peer to Peer Lending or unsure of it, but it’s really just a fixed income investment.

Fixed income is a necessary and important part of portfolio building and portfolio management, yet the options you have available for making fixed income investments are not many and not great.

You need to be sure you are properly compensated for the risks being taken.

The most widely available fixed income investment option for building a portfolio is a bond. There are different types, many of which are publicly traded.

Let’s look at some of these fixed income options and see how they compare…

Long Term Government Bonds

It doesn’t seem like that long ago when government bonds were considered the ‘risk free’ investment. Portfolio calculations of risk took the risk premium based on the actual or potential returns over and above Treasuries. After all, the US Government was never going to default on a debt, right? Well that used to be true. Confidence in our government to do anything seems to be shaken at the moment and that lack of confidence extends to government bonds and how they might perform in the future.

The longest term US Government Bond, the 30 year, has a rate that is right around 2.5%. This is low by all historic standards.

Today, inflation is near 1%. This means a real interest rate of 1.5%. Is that rate high enough to compensate you for the risk of holding onto a government bond for 30 years?

For most people it isn’t. Long term government bonds are an option but a not great one when it comes to balancing the risk/reward ratio.

Summary

Type: Long Term Government Bond

Term: 10 to 30 years

Risk: Moderate (higher than people think it is). Greatest risk is not keeping up with inflation.

Quality of Investment: Returns not great for real risks involved and very long term required to hold.

Sovereign wealth funds, governments and endowments need to keep buying Treasury bonds as it is one of the only markets large enough to absorb all the buying they have to do to put that money to work. Even at these paltry interest rates….

We are not a sovereign wealth fund. We have more choices…

Short Term Government Bonds (T-Bills)

T Bills have much shorter terms ranging from one month to one year. Rates for one-month T Bills are 0.254% and for one year are 0.642%. With an annual inflation rate of 1% we have a nominal real rate of return on the one-month T Bills and are losing money to inflation if we hold T Bills for one year.

One-year T Bills are obviously not a great investment.

The one month at 0.254% monthly over 12 months does give you a positive real rate of return on your money (3.048% -1% inflation), but some of that return is eaten up with transaction costs since you have to buy new T Bills each month meaning 12 transaction costs per year.

Summary

Type: T Bills (Short Term Government Bonds)

Term: up to 1 year

Risk: Low

Quality of Investment: The shorter the term, the better and a good place to park cash for a short period of time. One year has a negative real interest rate.

T Bills have their place especially for holding cash in a short term, temporary way while waiting to deploy funds into a more effective long term investment.

Now that we have looked at US government bonds, let’s look at some more options…

Corporate Bonds

If you are on a quest for yield, the US Government as bond issuer is probably not the place for you. We’ve seen that they don’t do great on our risk/reward scale either.

Since large companies issue bonds too, we need to give corporate bonds a look.

Corporate bonds are underwritten by a bank and issued with a rating from one of the 3 big rating agencies: S&P, Moody’s or Fitch. Corporate bonds should be a higher yield option for the fixed income portion of a portfolio. Yields on corporate bonds have been in steady decline over the last few years too.

A quick glance at some corporate bonds from the NY Times show some bonds by rating.

For instance, Oracle, who is AA- rated by S&P is yielding 1.9% on a 5 yr bond. AT&T, who is BBB+ rated by S&P, is yielding 4.68% on a 30 yr bond. Lastly, Cisco Systems, rated AA- by S&P is yielding just a hair under its coupon of 2.5% on a 10 yr bond.

To find a double digit yield, we had to search for a D rated (by S&P) bond with a 2022 maturity for Chesapeake Energy (CUSIP: CHK4116807) to find a yield of exactly 10.00%. A D rating means they have already failed to pay on at least one of their other obligations and a default is likely. A 10% rate is not exactly how you (or we) should be compensated for that kind of risk. And we have to hold this bond and hope they pay for 6 more years.

If you want to gamble you should go to Vegas, not gamble just to earn 10%.

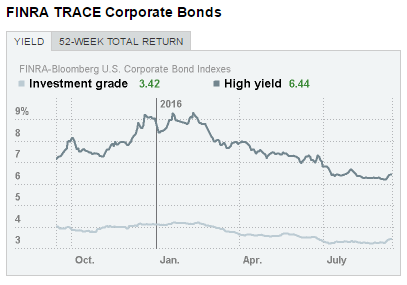

This chart from the NY Times shows yields for investment grade and high yield corporate bonds:

As you can see, rates are very low at 3.42% for investment grade and 6.44% for high yield, which are normally referred to as “junk” bonds. These rates are pretty slim for the risk we are taking. They do present some yield over and above US Gov’t bonds though.

Remember we are in a historically low interest rate environment. For all of these bonds, but especially corporate bonds, if interest rates rise then the value of our bonds will fall.

Who knows how long these historically low interest rate levels will last?

Summary

Type: Corporate Bonds

Term: Up to 30 years

Risk: Moderate on Short Term, High on Long Term and Junk

Quality of Investment: Investment grade bonds especially in the short term are probably solid. The longer the term and higher the yield the more uncertain due to rate environment and poor credits on the junk bonds.

If government bonds and corporate bonds are either low yielding or too low yielding for the risk you are taking, then how do you allocate the fixed income requirement of building your portfolio?

Peer to Peer/Marketplace Loans

To be a good fixed income investment, we need something that encompasses borrowing and steady repayment over time. We need to be able to select the type and average term of the loans we want.

And we need to be compensated for risk.

Peer to Peer loans are like a bet on a specific part(s) of the US economy. There are platforms that only do small business lending, or student loan refinancing or prime borrower (the best credits) unsecured consumer lending. US consumer lending is so large that if it was a country it would have the world’s 6th largest GDP.

In this space, Lending Club gets the most looks and the most talk because they have been publicly traded for a while now. They were also the industry darling before their springtime loan scandal and shakeup of the executive team that resulted. They are not the only platform out there.

Prosper, who is privately held, swims in the same pool that Lending Club does. Funding Circle and Dealstruck are small business lenders. P2BInvestor does business receivables financing. Realty Mogul, Fundrise and Patch of Land do real estate lending.

Many of the loans originated on the real estate platforms have 12-18 month terms for property rehab/renovation, and the consumer platforms are usually 36 or 60 month terms. Investments on different platforms can help you get the fixed income duration you are seeking, and spread the risk around too.

Whether the loan is secured by assets or not, nearly every platform has interest rates above 5-6%, and often in the double digits.

Funding Circle says the average investor can expect a rate of 7.3% after fees and non-payments. Dealstruck’s average rates are 10%-18%. Lending Club’s lowest rates are 5.32%-8.59% for A grade.

So how do we choose which platforms, and how do we invest wisely?

If you are not an accredited investor, you have more limited choices for how to invest your money in loans. Only Lending Club, Prosper and those that fund their loans through Reg A+ offerings. like Ground Floor are open to unaccredited investors.

If you are an accredited investor then many of the lending platforms are open to you but it can be hard to keep track of all the accounts and how much money is moving around, let alone all the logins and passwords.

So let’s sum it up compared to our other options…

Summary

Type: Peer to Peer Loans

Term: 12 months to 5 years (usually)

Risk: Low on the Excellent Grades (A grades and up), Higher as you go to lesser credit grades

Quality of Investment: More flexibility and versatility for portfolio building based on risk, duration, rate. Some diversification as money is spread over many borrowers. Go get higher rates and the defaults that come with it or get lower, slower steadier rates or mix and match. The risk/reward works here. Does not correlate with other financial markets.

One of the common concerns of Marketplace/Peer to Peer loans is that the industry has not experienced an economic downturn. The other fixed income options won’t do so well with a drastic turn of economic events either. Corporate bonds in particular will do very badly when the next recession hits. Government bonds would get more attention and buying interest but bid up bonds mean even lower rates and negative real rates for certain.

If you are like most people, then you don’t know how to analyze small business credit, individual personal credit or analyze financial statements. Maybe you do know how and you just don’t want to go through all that. So how do you select which loans to buy for your portfolio? It can be daunting.

That’s why one of the best and most diversified solutions for investing in Peer loans is…

A Managed Fund

For accredited investors there are some private investment funds that are dedicated to only invest in loans from the various online lending platforms.

It’s like a mutual fund but not of stocks or bonds, but of marketplace loans. Unlike a mutual fund, it’s a private investment fund and not public.

Like with stock mutual funds or ETFs where you buy diversification with smaller dollars, a managed fund is providing fixed income from many peer lending sources, not just one platform like if you had to pick loans yourself.

One of the best and most visible in the marketplace lending industry is Prime Meridian. They are a family of private funds that offer industry specific investing options covering multiple types of marketplace loans.

It’s possible to diversify across different sets of borrowers, different loan purposes, different loan amounts and different loan terms, all with one investment in one place, a managed fund.

Conclusion

As investors, you understand that fixed income is an asset class you need to have in your portfolio, somehow. It moves in unrelated ways to the stock market, which is important. But profitable, good yielding risk appropriate options for fixed income investment are few.

Look at Marketplace Lending.

If you want to diversify some of your portfolio into this one area of fixed income, then a managed fund is one way you can add this emerging asset class to your portfolio without all the hassle of picking loans and platforms yourself. The professionals handle it for you.

Generate income from your fixed income portion of your portfolio where you can earn real returns that outpace inflation and take a slice out of one of the biggest markets in the country.